War-risk surcharges, route diversions and port congestion threaten India’s export margins, especially for basmati and perishables. The ongoing West Asia war has quickly turned into a supply-chain shock for Indian exporters, with an estimated 40,000–45,000 export containers stranded across sea lanes and foreign ports, and cargo worth roughly 1–1.5 billion dollars now facing either diversion, costly delays or even a forced return home.

Industry estimates suggest that about 80 per cent of these containers are already at sea, underscoring how abruptly the conflict around the Strait of Hormuz has disrupted what was, until recently, a relatively stable export corridor.

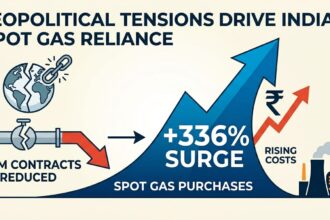

At the heart of the crisis is a steep escalation in war-risk pricing. Exporters report that, over and above normal freight of about 800–1,500 dollars per container on these routes, they are now being billed an additional 3,000–5,000 dollars in emergency conflict-related surcharges, taking total logistics costs up by three- to five-fold on some lanes. These extra levies include emergency cost recovery charges, contingency and peak season surcharges, imposed within days of the latest flare-up in the Hormuz region, as global carriers reassessed risk and rerouted vessels away from sensitive waters.

The impact is particularly acute for exporters of perishable and agri-based cargo, for whom time lost often translates into total loss. A large share of the stuck consignments is basmati rice, with close to 400,000 tonnes now immobilised in a three-node chain: at Indian ports, in transit and at destination-country ports in West Asia.

For these shippers, the combination of delays, rising storage costs and quality degradation is wiping out margins, even as they continue to face payment uncertainties from buyers in a war-affected region.

The logistics ecosystem itself is under severe strain. Trade-policy analysts and freight forwarders point out that some insurers have either sharply raised war-risk premiums or cancelled cover for vessels entering the conflict zone, effectively constraining capacity and forcing ships to either discharge cargo at alternate ports such as Salalah in Oman or sail back to India under force majeure conditions.

Non-Vessel Operating Common Carriers, which own containers but not ships, are also heavily exposed, as their boxes remain scattered across the Persian Gulf network with limited control over vessel deployment.

These disruptions are feeding back into India’s domestic port system. The shipping ministry is monitoring congestion closely, with around 20,000 containers reportedly stranded or awaiting evacuation at major state-owned ports as of early March, alongside roughly 700,000 tonnes of liquid bulk and nearly a thousand tonnes of perishable cargo stuck in storage.

Port authorities are considering easing rules and levies under the “back-to-town” customs provision, which allows exporters to pull cargo back into the domestic market to avoid mounting demurrage, detention and warehousing charges.

For some sectors, the pain is more about cost than absolute blockages. Apparel exporters, for instance, are not yet facing heavy war-risk surcharges but are seeing a sharp jump in freight due to longer, circuitous routes as ships avoid high-risk waters, with rates rising about 40 per cent from roughly 200 rupees per kilogram to 280 rupees per kilogram.

Maritime intelligence firm Drewry warns that if the crisis persists, base freight rates could also rise more broadly as port congestion, rerouting and longer rotations tie up vessels and equipment, tightening effective capacity on key east–west trades and making spot rates more volatile.

Overlaying this container crunch is a wider macro risk for India. The Strait of Hormuz and the Bab-el-Mandeb together sit astride more than half of India’s export corridor, and a prolonged disruption could put as much as 244 billion dollars of outbound trade at risk, while also threatening 35–50 per cent of India’s crude oil inflows that transit these chokepoints.

Ratings agencies such as ICRA have already warned that a sustained conflict could push up oil prices, widen India’s net import bill by tens of billions of dollars and strain the current account, with knock-on effects on corporate profitability and investment sentiment.

In the near term, exporters appear to be pursuing three imperfect strategies: absorbing part of the war-risk surcharges to honour contracts, negotiating shared cost burdens with overseas buyers and increasingly resorting to back-to-town options for high-risk and low-margin cargo.

Over time, the ability of firms to hold on will depend on how long the conflict lasts, how quickly insurers and container lines recalibrate risk, and whether the government can cushion the blow through regulatory forbearance at ports and targeted support for sectors such as basmati, processed foods and small manufacturers heavily reliant on West Asia routes.