Reserve Bank of India (RBI) Governor Sanjay Malhotra has reaffirmed India’s inflation and external debt are under control even with the persistent global shocks that affect global economies, highlighting the resilience of India’s macroeconomic environment.

During a dialogue at the Consulate General of India in New York, Malhotra said that India’s fundamentals, backed by a robust financial sector and progressive reforms, continue to bolster investor confidence on the nation’s growth prospects. The governor’s comments are delivered against a backdrop of growing uncertainty in the global economy amid geopolitical risks, trade disruptions and price volatility in critical commodities, especially oil prices.

Malhotra explained that India’s foreign exchange reserves, currently at around $700 billion, not only serve as a cushion against external shocks but also demonstrate sound economic stewardship. He also said India has increasingly become an integral part of the global economy, with the successful negotiation of eight free trade agreements with 37 countries, adding to its global trade participation. In the meantime, the maturation of the government and corporate bonds markets in India has increased the stability of financial markets and created opportunities for investment, making India a more popular destination for foreign investment. The RBI Governor also highlighted the regulatory efforts to enhance ease of access and efficiency for foreign investors, underscoring the country’s efforts to ensure a transparent and conducive environment for all investors.

But notwithstanding these positives, Malhotra warned that global risks are building and could make inflationary dynamics more challenging. In the minutes of the Monetary Policy Committee meeting on April 8, he noted several new risks, including escalating geopolitical tensions in West Asia, increasing international energy prices, and cost pressures, all of which have the potential to push up inflation. Further, the emergence of El Niño-like conditions could adversely affect crop production and exacerbate food price pressures in the months ahead. Malhotra characterised these elements as supply-side shocks that are not directly influenced by the conduct of monetary policy but can play a crucial role in affecting the price and growth, both for the country and the world.

He pointed out that the potential persistence of geopolitical tensions could adversely impact global supply chains in ways that were not envisaged earlier, slowing down the process of normalisation of supply chains. These factors not only pose risks to inflation, Malhotra said, but also risks to growth, posing a conundrum for central banks around the world. According to Malhotra, this makes inflation expectations even more challenging to manage, as central banks face the challenge of containing inflation while avoiding a potentially larger expansionary impact on the economy. This, he said, makes the central banking task a “arduous one”, particularly if disputes are left to linger.

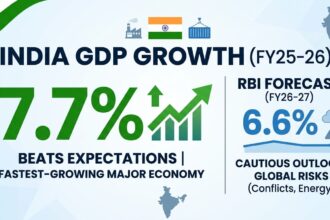

Despite such apprehensions, the RBI continues to claim that inflationary pressures in India remain well anchored when taken into account with global shocks. According to the central bank, the Monetary Policy Committee (MPC) in its recent meeting left the policy repo rate at 5.25%, suggesting a stable but cautious approach to monetary policy. The growth forecast for India has been revised down from 7.6% in FY26 to 6.9% in FY27, suggesting that the country is facing some global challenges, but at the same time is still expected to achieve strong growth compared to the international community. On the inflation front, the headline retail inflation is likely to average 4.6% this fiscal year, remaining within the RBI’s inflation target band, while the risks remain skewed upwards.

On the global front, the war in West Asia is already having negative supply-chain effects and raising prices. The MPC said these factors pose an “unprecedented challenge” for the global economy, as they simultaneously push up inflation and slow growth. Against this background, India’s comparatively lower volatility in macroeconomic indicators, healthy foreign exchange reserves and pre-emptive monetary and fiscal policies make it better placed than most countries to deal with such shocks. Malhotra emphasised that risks remain but that the Indian economy is currently in much stronger shape than before in global uncertain times, and will be able to wither such challenges.