India’s export story in October reads like a tale of two economies: on one side, smokestacks and refineries humming for the US; on the other, thousands of workers in diamond-cutting units, jewellery workshops and garment factories wondering why orders are drying up. How can exports be booming and struggling at the same time? The answer lies in the sharp divergence between energy and high-tech exports on the one hand, and labour-intensive sectors on the other.

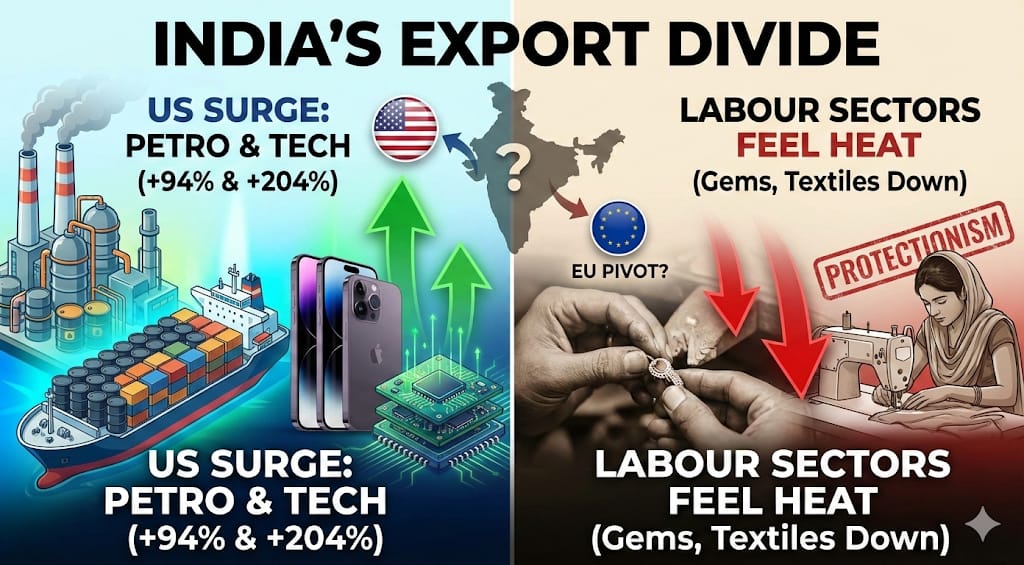

Petroleum exports to the US jumped a staggering 94.5 per cent in October, touching $251.5 million dollars. Why is this significant? Because in a month when most major categories faltered, petroleum stood out as almost the lone bright spot, and its partner in resilience was an unlikely ally: iPhone-led telecom instruments, which skyrocketed by 204 per cent. Does this mean India is quietly recasting its export profile to the US? The numbers suggest exactly that.

Ironically, this surge in petroleum exports to the US comes at a time when some of India’s traditional refined fuel markets are sharply cutting back. Why would the Netherlands slash purchases by 15.7 per cent, Australia by 93.1 per cent and Togo by 62.3 per cent? The reasons range from shifting sourcing patterns to changing refining economics and possibly geopolitical recalibrations, but the net effect is clear: what India is losing in some markets, it is partially compensating for in the US.

Yet, can petroleum alone carry the burden of India’s export ambitions? Not when labour-intensive sectors, which provide the bulk of jobs, are under strain. Gems, jewellery and garments, long the backbone of India’s employment-intensive export story, are slumping under tariff pressure and rising protectionism. This raises a crucial question: if the sectors that employ the most people are hurting, can a few high-value categories offset the social and political cost of this slowdown? The answer, uncomfortably, is no.

At the same time, the boom in telecom exports tells a parallel story about India’s evolving place in global value chains. Why are telecom instruments, especially iPhone-linked shipments, surging by over 200 per cent? Because the global de-risking from China is turning India into a key assembly and manufacturing base for premium electronics. When a device assembled in India ships out to the US, it nudges the trade narrative from “back-office services exporter” to “hardware manufacturing partner.”

Does this shift matter beyond just numbers? Absolutely. It signals that India is climbing up the tech ladder, but it also highlights a new vulnerability: being deeply embedded in global supply chains makes the country more sensitive to tariff wars, export controls and political fluctuations. If tariff tensions escalate further, could even these sunrise categories feel the heat? History suggests they very likely could.

This is where the diplomatic and trade choreography in New Delhi enters the frame. As India grapples with tariff headwinds in the US, External Affairs Minister S Jaishankar’s meeting with European Trade and Economic Security Commissioner Maros Sefcovic signals a strategic pivot: can a robust India-EU Free Trade Agreement counterbalance rising uncertainties elsewhere? The negotiating teams from India and the European Union are back at the table for two days of intense discussions, but this is no simple replay of stalled talks from a decade ago.

EU Ambassador Herve Delphin describes it as “EU-India FTA negotiation 2.0.” What does that mean in practice? It means both sides are consciously shedding the baggage of the past and treating this phase as a fresh negotiation, driven by a “growing sense of shared necessity and complementarity.” In other words, it is less about abstract trade theory and more about survival and advantage in a world of tariff wars and fractured supply chains.

Delphin’s framing is stark and strategic: if India and the EU together account for roughly 25 per cent of world GDP and 25 per cent of global demography, does an FTA between them really matter for the wider world? The answer, by his own admission, is yes – it “has a bearing.” In a global landscape where tariff offensives are becoming the norm and trade disputes dominate headlines, both partners see value in a predictable, rules-based economic framework.

Why the urgency now? Because businesses, investors and workers need stability to plan, and an FTA is one of the few tools that can still provide a degree of certainty. The EU’s track record, Delphin argues, shows that its FTAs are “win-win,” boosting trade, jobs and investment for both sides. Is that just diplomatic optimism, or hard-nosed economic calculation? Given how integrated European value chains are, and how hungry India is for technology, capital and markets, it is closer to the latter.

Perhaps the most telling shift is in the style of negotiation itself. Instead of the old model of slow, formal “rounds,” both sides have moved into a “continuous negotiating mode,” with around 40 European negotiators landing in Delhi to thrash out details. Does this signal that both sides are genuinely serious about closing a deal by year-end, as Delphin claims? The intensity suggests so, but the final outcome will depend on how deftly they bridge gaps on tariffs, standards, digital trade, sustainability and market access.

For India, the stakes go beyond percentages on a spreadsheet. Can a well-designed FTA with the EU open new high-value markets for sectors currently under pressure, like garments, gems and jewellery, while simultaneously locking in gains for telecom and energy-linked exports? If policy aligns with strategy, the answer could reshape India’s export map over the next decade. In the meantime, October’s data offers a preview of the crossroads: an India powered by petroleum and iPhones abroad, yet anxious about the fate of its traditional export workhorses at home, looking to Brussels as much as Washington to steady its trade future.