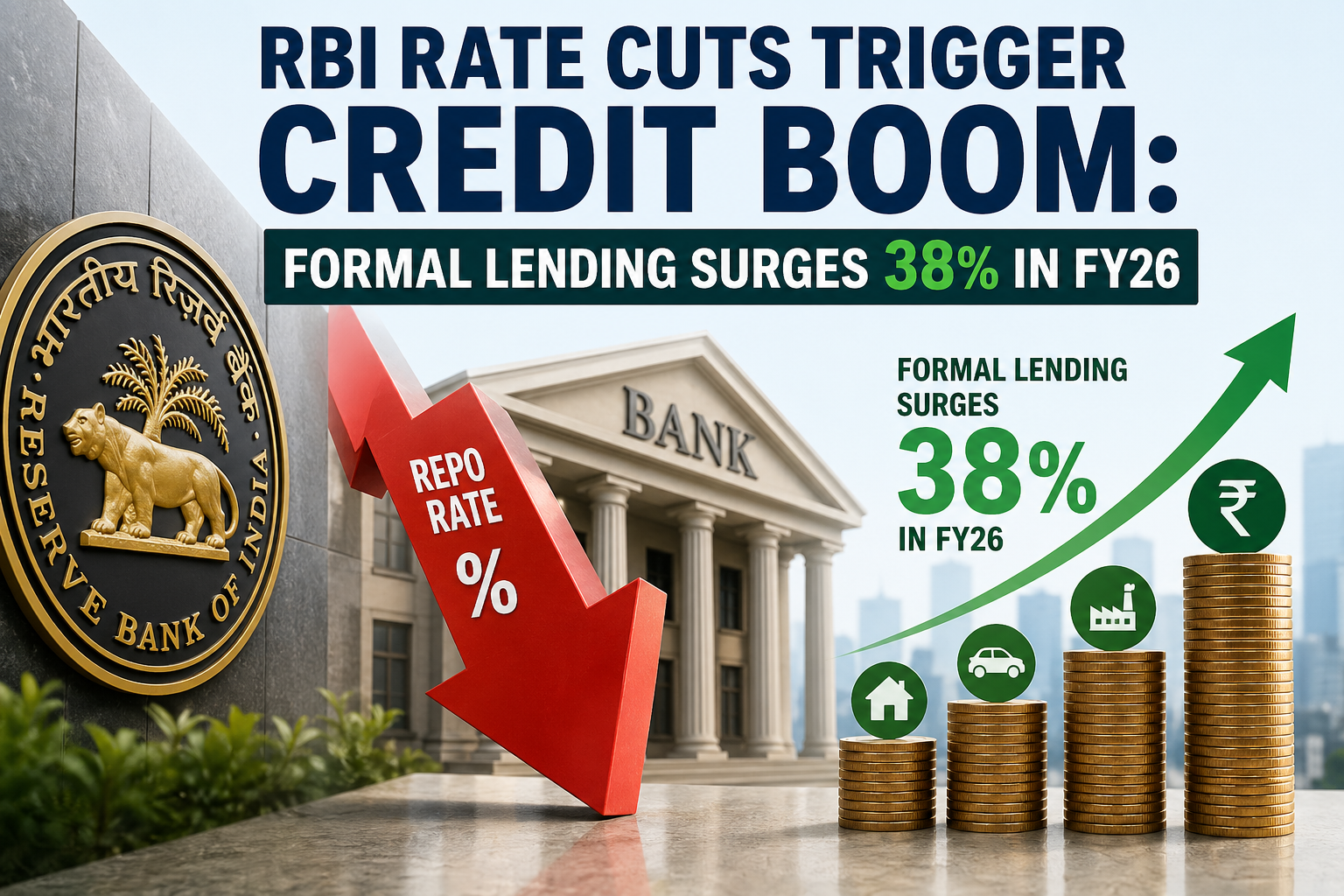

India’s credit cycle has made a sharp turnaround in FY26, with formal credit flows surging by 38% after an 8% contraction the previous year, signaling a strong revival in economic activity and borrowing appetite.

According to Reserve Bank of India data, total credit expansion rose to ₹44.6 lakh crore in FY26 from ₹32.3 lakh crore in FY25, marking one of the fastest recoveries in recent years. This rebound comes at a time when monetary policy turned decisively accommodative, setting the stage for cheaper borrowing and improved liquidity across the financial system.

The most significant trigger behind this surge has been the RBI’s aggressive easing cycle that began in February 2025. The central bank reduced policy rates by a cumulative 125 basis points, complemented by a 100 basis point cut in the cash reserve ratio.

Alongside this, the RBI injected ₹8.8 lakh crore of liquidity through government bond purchases, ensuring that banks had enough funds to lend. This coordinated policy push translated effectively into lower borrowing costs, with lending rates declining by 87 basis points to around 9% in February 2026 from 9.87% a year earlier, making credit more accessible to both businesses and consumers.

The impact of these measures is visible in the sharp expansion of non-food credit, which rose 16% year-on-year to ₹213 lakh crore as of March 31, 2026. This reflects robust demand from sectors such as infrastructure, manufacturing, and services, which are typically sensitive to interest rate movements.

At the same time, the overall outstanding flow of financial resources to the commercial sector crossed ₹300 lakh crore for the first time, reaching ₹311.8 lakh crore, growing at 15.8% compared to 11.7% in FY25. This milestone indicates not just cyclical recovery but also structural strengthening of credit intermediation in the economy.

Interestingly, the credit revival has not been limited to traditional bank lending. Non-bank sources also played a crucial role, with total resource mobilization from these channels rising 15.6% to ₹99 lakh crore. Domestic sources accounted for a significant share, increasing 17% to ₹73.2 lakh crore, while foreign borrowings grew 12% to ₹25.6 lakh crore.

Among domestic non-bank channels, non-banking financial companies emerged as the largest contributors with ₹3.62 lakh crore in flows, followed by equity issuances worth ₹3.45 lakh crore and corporate bond issuances of ₹3 lakh crore. This diversified funding pattern suggests a maturing financial ecosystem where businesses are increasingly tapping multiple channels beyond banks.

Foreign capital flows also saw a notable uptick, reinforcing investor confidence in India’s growth story. Funds raised from foreign sources jumped 50% to ₹4.91 lakh crore during FY26, driven largely by a rise in foreign direct investment, which increased to ₹3.24 lakh crore from ₹2.17 lakh crore in the previous year.

This surge indicates that global investors are responding positively to India’s macroeconomic stability, policy reforms, and growth prospects, even amid uncertain global conditions.

The broader implication of this credit expansion is a likely boost to economic growth momentum going forward. Increased credit availability typically supports capital expenditure, consumption, and business expansion, creating a multiplier effect across sectors.

However, sustainability will depend on the quality of credit growth, asset quality trends, and global financial conditions. If managed well, the current cycle could mark the beginning of a more durable investment-led growth phase for the Indian economy.

As India navigates a complex global landscape, the FY26 credit surge underscores the effectiveness of timely monetary intervention and the resilience of domestic demand. The coming quarters will reveal whether this momentum translates into long-term structural gains or remains a cyclical upswing driven by policy stimulus.