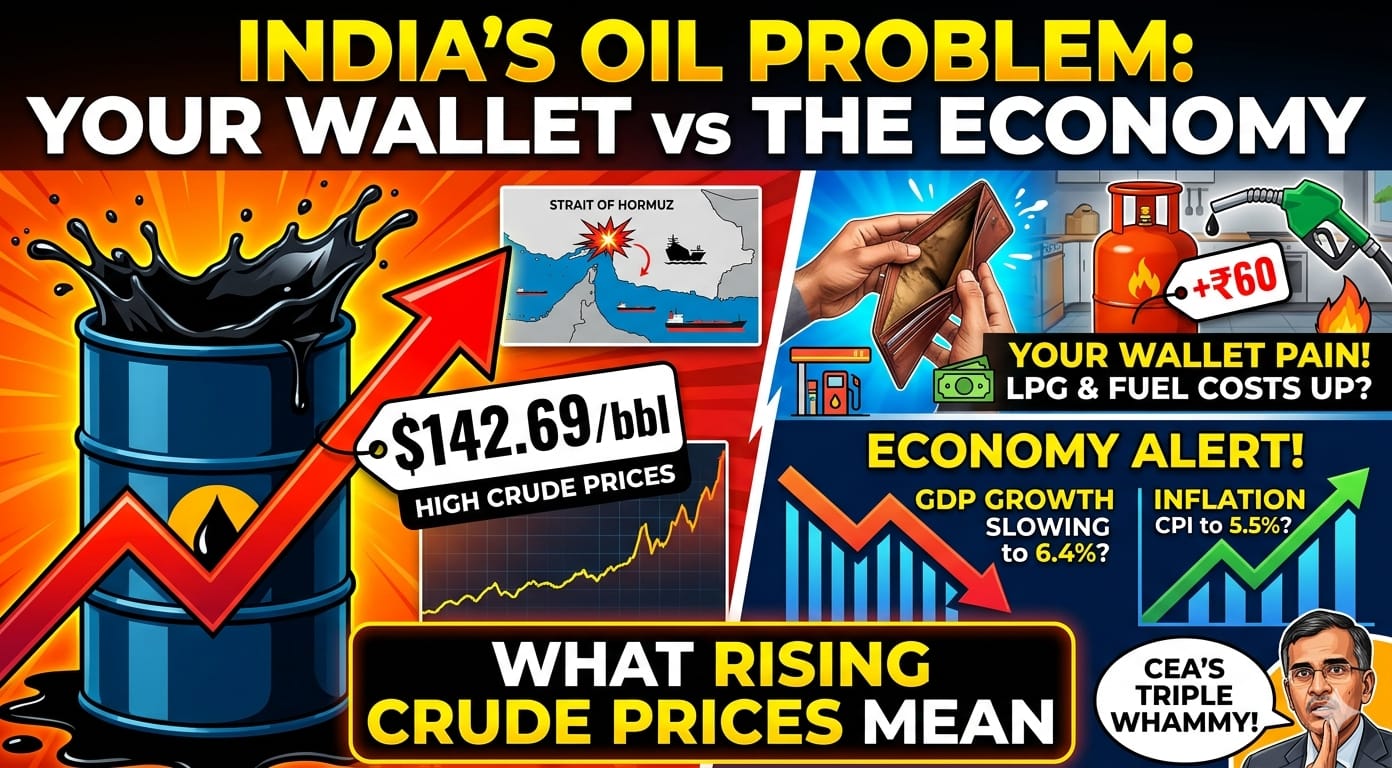

To understand why India’s top economist recently went before Parliament with some very specific numbers, you first need to know one thing: India imports about 88% of its crude oil needs from global markets. That makes the country deeply sensitive to any price shocks in global oil. And right now, there is a very big shock underway.

The trigger is the ongoing conflict in West Asia. As the US-Israel war with Iran entered its third week, the movement of crude oil and natural gas through the Strait of Hormuz — the narrow waterway connecting the Persian Gulf with the Gulf of Oman — has been severely impacted. Close to 20% of the world’s crude oil, natural gas, and liquefied petroleum gas is shipped through this chokepoint. Almost half of India’s crude oil needs and 20% of its gas pass through the same route. When that route gets disrupted, India feels it — hard.

It was against this backdrop that Chief Economic Advisor (CEA) V. Anantha Nageswaran appeared before Parliament’s Standing Committee on Finance on March 2, 2026. The committee had asked him a sharp question: how does the government plan to handle what they called a “triple whammy” — rising crude oil prices, market volatility, and maritime delays caused by the West Asia conflict? Nageswaran’s response was methodical.

He told the committee that his team had run simulations at three different price levels — $90, $110, and $130 per barrel — to see how each scenario would affect the Indian economy. His key message was this: up to $90 per barrel, India’s macroeconomic targets for FY2026-27 remain intact. GDP growth of 7–7.4%, inflation around 2%, a current account deficit of 1–1.2%, and a fiscal deficit of 4.3–4.4% would all still be achievable.

At that level, the impact on the broader economy would be, in his own words, “almost insignificant or not relevant.” But the picture changes sharply at higher price levels. If oil stays at $130 per barrel for two to three quarters, retail inflation (CPI) could spike to 5.5%, GDP growth could fall to 6.4%, the current account deficit could widen to 3.2% of GDP, and the fiscal deficit could balloon to 5.6% — numbers that would seriously strain India’s finances and household budgets.

Now, even as Nageswaran was presenting this analysis, crude oil prices were already moving well beyond the “safe” $90 threshold. As of now, these are the rates: India’s crude oil basket touched $142.69 per barrel on March 16 — more than double the $70 per barrel that prevailed when the war started on February 28. While $108.23 is the average for March.

To put that in context, the average price of India’s crude oil basket for March stood at $108.23 per barrel — up 57% from February — even before the latest spike was fully factored in. Now, what remains to be seen is what the average rate will be by the time the war ends.

Why is India’s basket price even higher than the global Brent or WTI benchmarks you hear about in the news? The Indian basket comprises roughly two‑thirds of the basket is sour‑grade crude from Oman and Dubai.The Iran conflict has driven up prices of Middle Eastern grades of crude, which form the bulk of India’s imports. Additionally, insurance and shipping rates for cargoes from the Middle East have risen sharply.

On the supply side, the government has been working to cushion the blow. Petroleum Minister Hardeep Singh Puri told Parliament that non-Hormuz sourcing has risen to approximately 70% of crude imports, up from 55% before the conflict began, and that India now sources crude oil from 40 countries, compared to just 27 in 2006-07. India also holds around 30 days of crude oil reserves. So while there is no immediate supply crisis, the price pressure is very real and building.

At the consumer end, petrol and diesel pump prices have not yet been hiked — the government has held the line there. But cooking gas has not been spared. The price of household LPG cylinders has been raised by ₹60, a move that economists estimate will push up retail inflation in March by around 12–13 basis points on its own. Meanwhile, the Reserve Bank of India had forecast GDP growth at 6.9–7% for the first two quarters of FY27, though it flagged “evenly balanced” risks — a phrase that sounds cautious today, given that oil has already crossed the $130 threshold the CEA described as the danger zone.

Now, what remains to be seen is what the average crude rate will be by the time the West Asia war‑related tensions ease. Right now, markets are already baking in a fair degree of risk, which is why prices are holding above $90/bbl and India’s basket is touching $108–109/bbl.

If the situation stabilises quickly and oil eases back towards the $90 zone, the macro impact on India should stay limited, as the CEA has suggested. But if hostilities drag on and crude remains materially above $100/bbl for a sustained period, the risks to inflation, growth and the fiscal deficit will only grow; in that case, the “almost insignificant” $90‑barrel scenario would no longer be the base case, and policymakers would be forced to recalibrate.