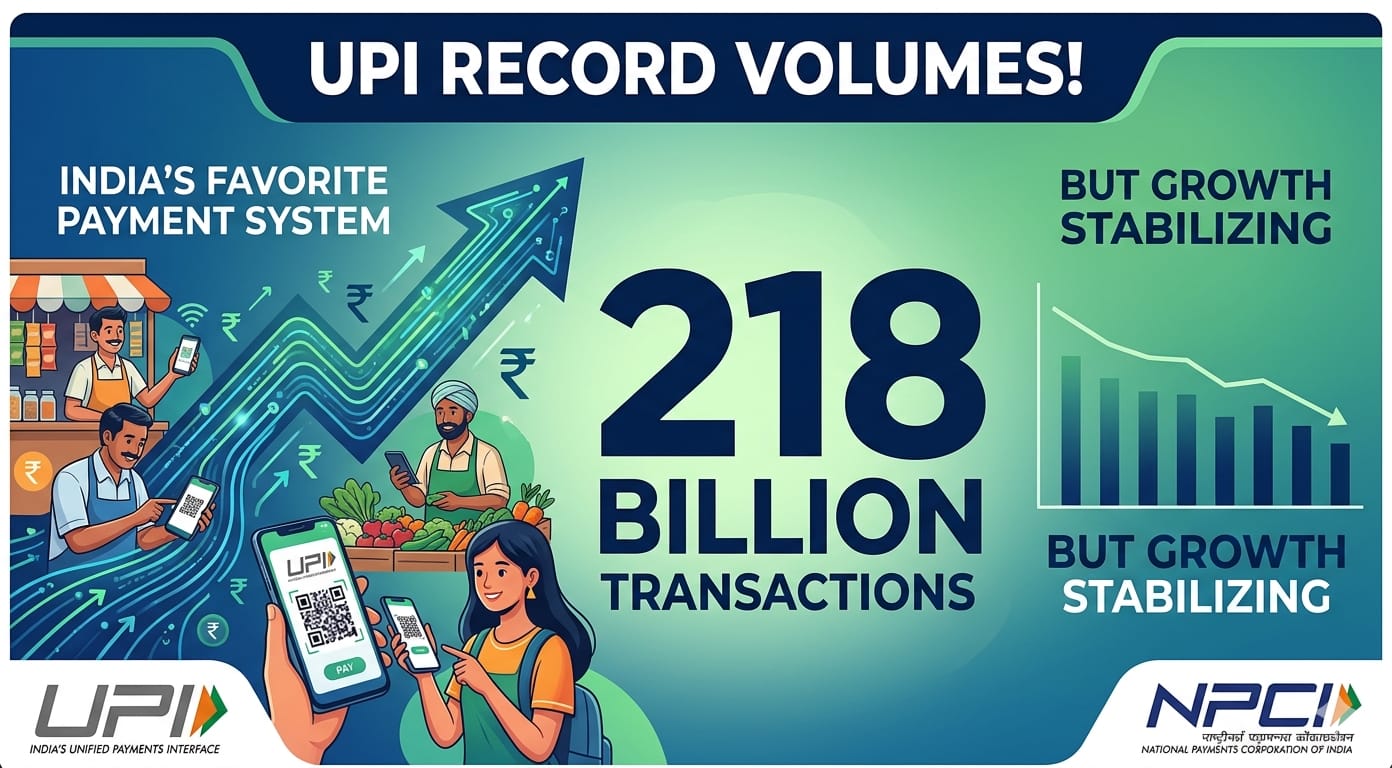

The Unified Payments Interface (UPI), India’s flagship digital payment system, continues to dominate the country’s cashless economy, having processed an impressive 218.6 billion transactions in the first eleven months of FY26. According to data from the National Payments Corporation of India (NPCI), these transactions carried a combined value of ₹284.7 lakh crore. The numbers reflect how deeply UPI has become a part of India’s daily life, from small shopkeepers and e-commerce payments to salaries and utility bills. However, towards the end of the fiscal year, there are visible signs of growth stabilising after two years of explosive expansion.

Through most of FY26, UPI transaction volumes stayed consistently high, exceeding the 20-billion mark in several months. January stood out as the best-performing month with 21.7 billion transactions, followed by December and October with 21.6 billion and 20.7 billion transactions, respectively. In terms of value, January once again led with ₹28.33 lakh crore, helped by strong year-end activities such as bonus payouts, holiday spending, and festive shopping. Analysts say this surge in transactions shows that UPI continues to play a vital role in both retail and large-value digital payments.

Yet, the performance in February 2026 pointed to a cooling trend. Transaction volumes slipped to 20.3 billion, while the total transaction value declined to ₹26.84 lakh crore. Industry observers say that while UPI has reached near-universal adoption across urban India, the slowdown could be an indication that the platform is now maturing rather than expanding at a breakneck pace. The next phase of growth may depend on deepening adoption in rural areas, the introduction of new payment features, or better monetisation models for payment providers.

When it comes to market share, the UPI ecosystem continues to be dominated by three key players — PhonePe, Google Pay, and Paytm. These apps control the majority of both transaction volumes and user base. However, competition is heating up as newer players like Navi, Super.money, and the BHIM app try to carve their space by offering faster payments, rewards, or specialized services. The entry of global giant Apple is also on the horizon, as it explores launching Apple Pay in India in partnership with major banks such as HDFC Bank, ICICI Bank, and Axis Bank. Despite these discussions, Apple faces challenges in adapting its business model to India, where UPI transactions are mostly free of cost and profit margins are thin.

The NPCI, which manages the UPI ecosystem, has also seen its own financials strengthen. In FY25, the organization reported a 41.7% rise in net profit (or revenue surplus) to ₹1,552 crore, with total income increasing 19% to ₹3,270 crore. While UPI operates as a zero-cost payment system for consumers and merchants, NPCI’s revenues come from other payment networks, services, and institutional partnerships. Its FY26 financial results are still awaited but are expected to reflect UPI’s continued expansion and operational growth.

Behind the scenes, however, India’s digital payments ecosystem has been receiving government support to sustain its zero-MDR (merchant discount rate) policy. Over the past four years, the government has disbursed around ₹8,000 crore in subsidies to banks and payment firms for UPI and RuPay debit card transactions. In FY25 alone, payments firms received ₹1,000 crore, against a sanctioned allocation of ₹1,500 crore — one of the lowest in recent years. For FY26, the subsidy release is still pending and likely to be finalized by the end of March.

Meanwhile, calls for reintroducing a merchant discount rate have grown louder in the industry. The MDR — a small fee paid by merchants to banks for processing transactions — could help create a sustainable revenue model for UPI stakeholders, especially as scale-driven growth begins to flatten. Earlier this month, the Standing Parliamentary Committee on Finance recommended a graded MDR framework to allow stakeholders to monetise digital payments without burdening small merchants.

Other retail payment systems such as the Aadhaar Enabled Payment System (AePS), Immediate Payment Service (IMPS), and Fastag have either slowed down or experienced marginal declines in usage compared to UPI’s massive footprint. Experts believe that while growth in transaction numbers may be stabilising, UPI’s dominance in India’s digital payments sector remains unchallenged. With new players, policy shifts, and possible technology integrations ahead, FY27 could mark the beginning of a new phase for India’s homegrown payment revolution.