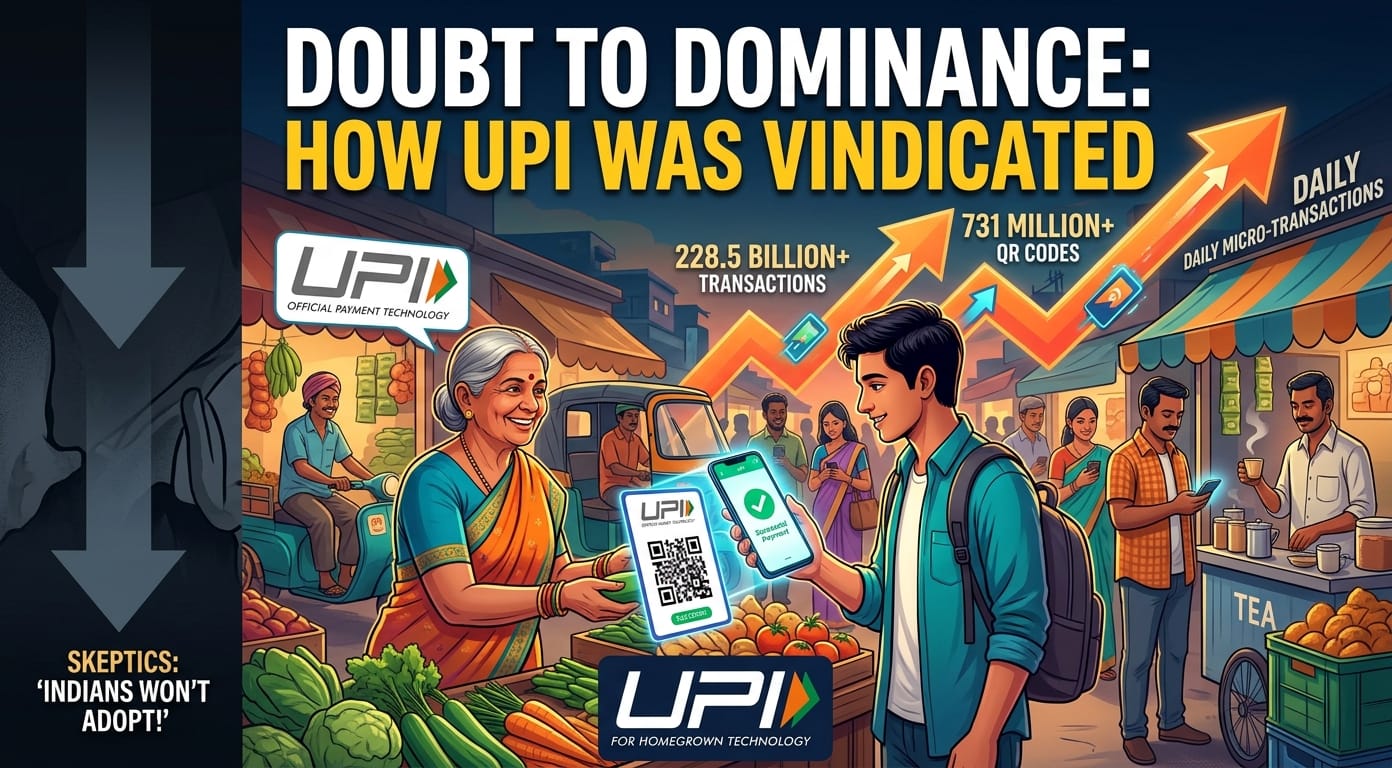

The Unified Payments Interface (UPI) was introduced in India with little belief that it will make it to where it is today, the savior of online payments. Children of skepticism: P. Chidambaram was the loudest supporter of skepticism, and once made fun of the notion that Indians were not going to adopt such a system in large numbers. Going way up to 2025, it looks as though even the figures themselves have risen to argue him absolutely wrong. UPI is not being used, it has become a habit, a culture and a statement of digital empowerment of India.

According to a recent report by Worldline, the UPI Quick Response (QR) codes increased by 15 percent in 2025 and the total was 731.38 million compared to 633.44 million a year earlier. Those little squares you can find on all the shop counters to-day, are no mere scraps of paper; they are a revolution. Whether it is vegetables sellers or tiny grocery stores, from major shopping malls to the small chai shoppers — everybody is digitizing by scanning and paying. What Chidambaram previously termed as impractical change has now emerged as one of the best Fintech success stories bringing about financial inclusion at a magnitude that few would have acquitted just some years ago.

The same report shows that the amount of UPI transactions increased by a colossal 33 percent and it has been surging towards 228.5 billion in 2025 compared to 172.2 billion in 2024. This not only transforms UPI into a payment method but also into a national movement. Interestingly, the more traditional Point of Sale (POS) terminals rose also on the 15 percent range to 11.48 million indicating that merchants were adopting the two types of digital acceptance. To citizens, however, UPI will still be the most preferable option to use; it is easy, quick, and it does not have the inconveniences of cards or money.

The average ticket price is among the most accurate predictors of user behaviour – the average amount that users are spending each time they shop. The average UPI payment in 2025 was 1,314 as compared to 1,437 the year before. The decline, although minute indicates that UPI is being used to make daily small-value payments – the type individuals use to purchase tea, groceries, go on auto rides or buy snacks. It demonstrates that digital transactions are not only big online purchases that are observed in everyday life. Conversely, credit cards cost on average ₹4,150 and debit cards 3,360 per transaction indicating that they are mostly a high-value or intended expenditure.

UPI is expected to outpace all the other payment modes soon not only in terms of quantity but its cultural effects as well, in case UPI continues its expansion rate. It was more than mere political commentary by Chidambaram but a mentality where the unskilled Indian with a wallet could not predict how technology would make money transfer easier. That same average Indian is today proving him wrong, second after second. In big cities such as Kolkata and Mumbai as well as small towns such as Bhagalpur and Surat, QR scanning is being done at a rate much higher than change counting.

UPI’s growth story is more than just data — it’s an emotional and practical shift. It has granted earthlings access to a digital economy at the same scale, enabled the young generation to conveniently spend money, and enabled millions of people to monitor and control costs. The reason why the home-grown system in India has done better than the payment technology of global giants is the strongest indicator that nothing (external validation) can inhibit innovation in this area.

Following the 2025 figures, the trust that India had in UPI cannot be dented, and each scan, tap, and transfer provides it with another chapter in the tale of overcoming the uncertainty. India made it unstoppable, Chidambaram said people wouldn’t use it but India didn’t just use UPI.